.jpg)

2025 is the year of MSC, the first major container shipping line without an alliance!

2024, a year in review...

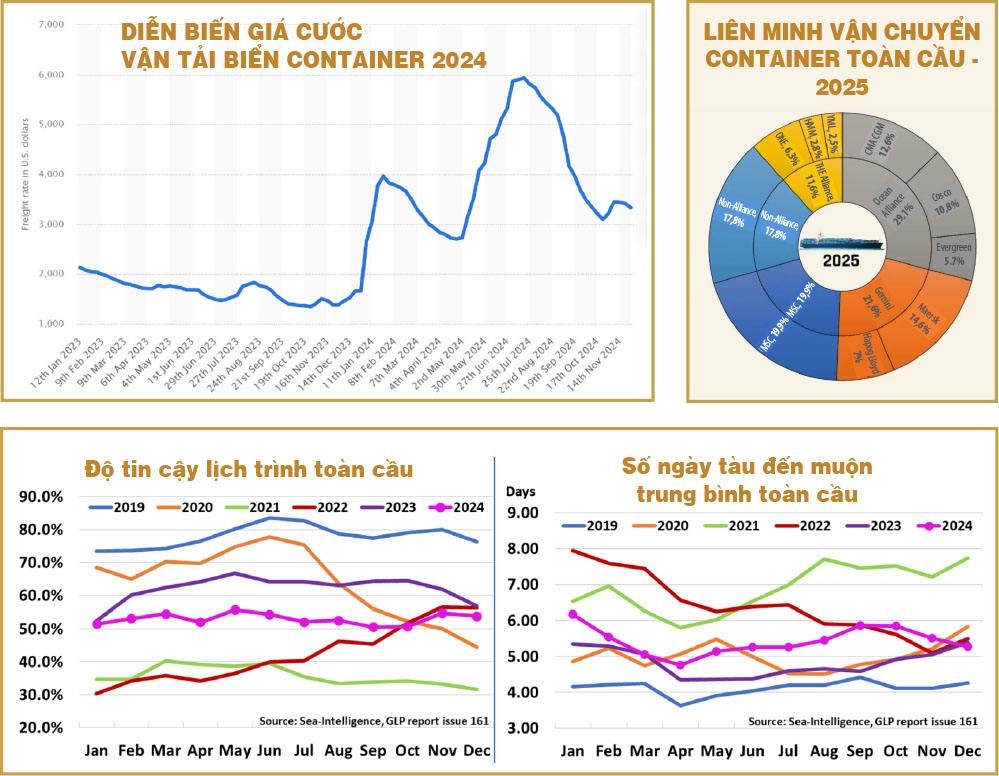

2024 marks a year of unexpected price increases for container shipping lines on the Asia-Europe/Mediterranean and Asia-North America trade corridors. According to Statista, from a low of US$1,342 per 40-foot container (October 26, 2023), rates have rebounded to a peak of over US$5,900 (June 2024) and dropped to US$3,331 (November 28, 2024).

The main causes come from geopolitical bottlenecks (Suez Canal with Red Sea crisis), climate change (Panama Canal) leading to chain congestion of some major ports in Asia, Europe and America on the East-West corridor. Linerlytica's report shows, "Global port congestion indicator reaches 2 million TEU, accounting for 6.8% of the global fleet".

Supply will continue to increase in 2025

Subjectively, although shipping lines are trying to delay new shipbuilding contracts to control supply, the actual supply increase from the number of new ships built in 2024 is 3.1 million TEU, more than last year's forecast of 2.95 million TEU (an increase of 150,000 TEU).

This year, the number of new ships delivered as planned is expected to have a total capacity of 1.9 million TEU, less than last year's forecast of 2.26 million TEU (down 360,000 TEU). However, this figure is equivalent to 6.3% growth for total new supply (30 million TEU). The top 12 shipping lines all increased their capacity, with growth of over 7%. In particular, MSC increased significantly by 692,000 TEU, reaching 12.3%.

Looking back at the trend over the past five years since the Covid-19 pandemic, total supply in the market has tended to increase sharply.

In terms of ship size, Alphaliner data shows that 90% (1.9 million TEU) of new construction has a capacity of 5,000 TEU or more. The number of large ships (15,000-18,000 TEU) is 55 and the number of super-large ships (over 18,000 TEU) is nine. This shows that the supply increase is mainly in the long-distance shipping routes between Asia - North America and Asia - Europe in the East - West corridor.

Will increased supply cause prices to fall?

In a recent development, according to The Loadstar, the Red Sea crisis showed signs of cooling down when the Houthis confirmed that they would stop attacking non-Israeli-owned ships and ships not flying the Israeli flag following the ceasefire and hostage exchange in the Gaza Strip.

What would happen if the Suez Canal route were fully restored?

Consulting firm Drewry forecasts that supply will exceed demand by 25% (about 1.8 million TEUs).

Xeneta, a leading platform for ocean and air freight rates, predicts that freight rates will fall by 11% compared to 2024 prices combined with an expected increase in demand in 2025, and this recovery will lead to chaos in operating plans as shipping schedules change across lines.

However, objectively, for more than a year now, shipping lines have maintained most of their shipping routes around the Cape of Good Hope.

According to Linerlytica's "Global Containership Port Congestion January 2025", congestion at major ports on the East-West trade corridor (Europe - Asia - America) is leading the list of nearly 30 major global ports that are congested. The top 10 include four ports in China (Shanghai, Ningbo, Shenzhen, Qingdao with 223 ships anchored waiting for berths); four European ports (Rotterdam, Netherlands; Antwerp, Belgium; Le Havre, France; and Algeciras, Spain with 66 ships); and two US East Coast ports (Savannah and Charleston, with 25 ships). The main causes are unfavorable weather conditions and high cargo volumes before the Lunar New Year, affecting 3.3 million TEUs of capacity or 10.5% of the total number of ships.

Will port congestion continue the trend of 2024, leading to high freight rates, inefficient vessel operations, and challenges to global supply chains?

Blank sailing has become a normal phenomenon in global container shipping due to objective and subjective reasons in recent years. According to Flexport, blank sailing in 2024 will be maintained at a fairly high level (15-20%), especially in the Asia-Europe trade route due to the Red Sea crisis and congestion of some major ports in these two continents. Blank sailing will still be an effective tool for shipping lines to control supply during times of reduced demand, causing market prices to always tend to be unstable.

Shipping line restructuring, a challenge for global supply chains

The year 2025 marks another milestone in the restructuring process that has continued throughout its nearly 30-year history. Except for the Ocean Alliance, which remains the same; Hapag-Lloyd leaves THE Alliance to combine with Maersk to form the Gemini Cooperation Alliance (February 2025); THE Alliance with its three remaining members has been renewed with the Premier brand (September 2024).

In particular, MSC will be the first major alliance-free container shipping line to account for a market share of up to 19.9%, equivalent to an alliance with the third-largest capacity after the Ocean and Gemini alliances. The world's largest Swiss container shipping line operates independently but will cooperate in slot exchange cooperation on nine Asia-Northern Europe and Asia-Mediterranean trade routes with the Premier Alliance; sign a three-year slot swap/vessel sharing agreement (VSA) with ZIM for six service routes from Asia to the US East Coast and Gulf, Mexico West Coast, and Caribbean ports; to compensate for lost routes for both parties (February 2025).

The disruption of alliances leads to disruption of shipping capacity and shipping routes. This will be a big challenge for importers and exporters.

Restructuring the shipping network

In early February 2025, Gemini Cooperation will introduce a new operating model, Hub-and-Spoke, reducing the number of hubs and increasing the number of feeders to many ports of departure and arrival (Spoke). In contrast to Gemini's model, also in February this year, MSC will launch an independent East/West network with a direct connection strategy, promising up to 1,900 direct port pairs without going through a transit hub. The other two alliances will continue to operate the traditional Point-to-Point (P2P) model.

With the new alliance structure, flexible service routes and diversified shipping network restructuring as above, importers and exporters will have more options for each product and their different transportation needs. However, the schedule reliability of the two new models Hub-and-Spoke and Direct connection will need time to be verified in an uncertain environment like today.

Will schedule reliability improve?

According to Sea-Intelligence, the on-schedule performance in 2024 is quite low, at 50-55% (an average delay of 5.28 days) compared to 2023 figures. The results of the past six years of monitoring show that schedule reliability has not recovered from the pandemic but is trending lower.

Moving into 2025, with fault lines such as the Red Sea/Suez Canal/Panama Canal, climate change with increasingly complex droughts, storms and floods, widespread port congestion, and current heightened geopolitical tensions on the objective side; changing alliances and changing the structure of the shipping network on the subjective side; improving the reliability of shipping lines' schedules is a huge challenge, especially the target of over 90% of Gemini Cooperation seems impossible.

Fitch Ratings has changed its outlook for global container shipping to “stable” from “deteriorating” in 2025 due to improvements in the tanker and bulk carrier markets. However, “shipping remains one of the most vulnerable sectors to geopolitical conflicts due to multiple chokepoints on key trade routes, its critical role in global supply chains, and its limited ability to adjust capacity effectively in the short term.”